FRANKFURT AM MAIN: Germany’s Lufthansa has warned that 30,000 jobs are under threat as it scaled down its winter schedule to levels not seen since the 1970s as demand for travel collapses because of the coronavirus pandemic.

The executive board of Europe’s largest airline said in a letter to employees that it was now “harder than ever” to predict how the aviation industry will develop, given there is little clarity over how long travel warnings would be applied or how quickly any recovery could come.

The use of video conferences may have also changed attitudes to travel against the backdrop of environmental prerogatives, while pressures on income could also weigh on tourism, the board wrote in the letter seen by AFP.

“No one can reliably predict these effects. We are determined nevertheless to preserve at least 100,000 of the Lufthansa Group’s 130,000 current jobs. Even if we do not currently have nearly enough jobs for a workforce of this size,” it added.

Lufthansa in September said more jobs would go beyond the 22,000 previously announced but did not give a clear figure then.

The German state in June stepped in to take a 25 percent stake in the airline, pumping nine billion euros of liquidity to prop up one of the nation’s most internationally visible companies.

The carrier – including its subsidiaries Swiss, Austrian, Brussels Airlines and Eurowings — said it would ground 125 more planes than planned in the winter, offering a maximum of a quarter of 2019’s capacity as it anticipates “less than a fifth” of the previous year’s passengers.

The season would be an “immense challenge,” it said.

“After a summer that gave us all reason for hope, we are now once again in a situation that is tantamount to a lockdown in effect.”

As the travel industry adapts to a post-pandemic world, the airline’s board said “we will be a smaller but also a more efficient Lufthansa. The road there will be long and arduous.”

The German flag carrier has succeeded in cutting its outflow of funds at the start of the pandemic from one million euros ($1.2 million) per hour to “only” one million euros every two hours, it said.

It will reduce administrative functions to around 30 percent, and shutter most of its main office in Frankfurt. Eurowings will entirely give up its office space in Dusseldorf.

The company will also keep employees on shorter work hours for a longer time — up to the end of February from mid-December previously.

Lufthansa reported an operating loss of 1.3 billion euros in preliminary third-quarter figures but the three months to the end of 2020 are looking far gloomier.

Lufthansa says 30,000 jobs at risk over coronavirus pandemic

https://arab.news/ykff9

Lufthansa says 30,000 jobs at risk over coronavirus pandemic

- Letter to employees says that it is now ‘harder than ever’ to predict how the aviation industry will develop

IsDB Group annual meetings conclude with 85 agreements worth over $8bn

RIYADH: As many as 85 agreements worth over $8 billion were signed across diverse sectors during the recently concluded annual meetings of the Islamic Development Bank Group.

This stands in contrast to the last year’s meetings, which recorded only 77 financing agreements, totaling $5.4 billion.

Speaking at the concluding press briefing, IsDB Chairman Mohammed bin Sulaiman Al-Jasser disclosed the signing of financing agreements between the group's institutions, 38 member countries, and 22 international financial institutions, covering diverse projects.

He lauded the continuous backing of the group by Saudi leadership, citing it as a testament to the Kingdom’s commitment to global cooperation and advancement.

Highlighting the significance of this year’s gatherings, the chairman mentioned that they included meetings of the IsDB Group’s councils and over 27 consequential side events.

These sessions brought together distinguished intellectuals, experts, and researchers from various developmental domains, with a total of more than 3,750 participants.

Notably, representatives from approximately 55 international and regional partner organizations, including 23 institutional heads, were present.

Detailing the Private Sector Forum’s activities, Al-Jasser noted the participation of over 1,500 delegates from more than 60 nations. The forum, comprising 17 events, facilitated the signing of over 60 agreements amounting to approximately $6.5 billion.

Over the past 50 years, the IsDB has played a significant role in progress by funding developmental projects exceeding a total value of $182 billion, according to the chairman.

These projects have encompassed diverse vital areas, ranging from basic infrastructure and agriculture to various strategic sectors such as health, education and energy, as well as trade, and Islamic finance.

He emphasized that the discussions and exchanges during the meetings provided valuable insights and success stories crucial for fostering sustainable social and economic development. He affirmed that the outcomes would transform the IsDB’s future initiatives and strategic partnerships.

The issuance of the “Golden Jubilee Declaration” by the IsDB Board of Governors, acknowledging the bank’s pivotal role and achievements, was also highlighted by Al-Jasser.

The declaration outlined key future priorities, including enhancing governance, expanding concessional financing, and advancing Islamic finance and cooperation in Southern countries.

In conclusion, Al-Jasser reiterated the theme of the annual meetings – “Cherishing our Past, charting our Future: Originality, Solidarity and Prosperity” – underscoring its significance as a guiding principle for the IsDB’s trajectory.

He emphasized the organization’s commitment to drawing inspiration from past achievements, learning from historical lessons, and leveraging current challenges and opportunities to forge a brighter future.

Last year, the IsDB Group announced several projects with 24 member countries aimed at addressing pressing challenges hindering growth in the Global South, with a focus on health, agriculture, and food security, as well as initiatives targeting small and medium enterprises, education, and humanitarian assistance, among others.

Saudi’s Ma’aden completes 10% acquisition of Brazil’s Vale Base Metals

RIYADH: Saudi Arabian Mining Co., also known as Ma’aden, has announced that it has completed the 10 percent acquisition of Brazil’s Vale Base Metals.

Ma’aden, which is majority-owned by the Public Investment Fund, said that its joint venture, Manara Minerals Investment Co., finalized the purchase, according to a Tadawul statement.

This move will boost the growth of the Kingdom’s mining sector in line with the objectives of the Vision 2030 initiative to diversify the Saudi economy away from oil.

It follows Ma’aden’s announcement in July 2023 that its joint venture had signed a binding agreement to acquire the stake for $26 billion as part of a strategy to invest in global mining assets.

“This investment is an important milestone for Manara Minerals. Through our investment in VBM, we are increasing the supply of strategic minerals and enabling Saudi Arabia to play a growing role in the global energy transition supply chains,” Robert Wilt, executive director of Manara Minerals and CEO of Ma’aden, said at the time in a statement.

“Our proactive approach is a step further towards Saudi Vision 2030. It will support local industrial development, create jobs across the Kingdom, and strengthen the position of the mining sector as the third pillar of the economy,” Wilt added at the time.

Egypt’s net foreign assets deficit shrinks $17.8bn in March

CAIRO: Egypt’s net foreign assets deficit shrank $17.8 billion in March, its second month of decline, central bank data showed, after remittances, foreign portfolio investment and a $5 billion payment from the UAE poured into the country, according to Reuters.

Egypt received a second $5 billion payment from the UAE in early March for a land development on the Mediterranean coast after an initial payment in February.

On March 6, it devalued its currency and announced an $8 billion agreement with the International Monetary Fund, triggering a flood of portfolio investments and remittances from workers abroad.

The March NFA deficit shrank to 200 billion Egyptian pounds ($4.18 billion) from 679 billion pounds in February.

The March NFA figures does not reflect an $820 million first instalment in early April under the expanded IMF financial support program.

Commercial banks’ foreign assets jumped by $7.4 billion in March while their liabilities slid by $3 billion, according to Reuters calculations based on central bank data and taking account of the March 6 devaluation.

Egypt has allowed its currency to weaken to 47.8 pounds to the dollar since it signed the IMF agreement after having left it fixed at 30.85 to the dollar for a year.

Central bank foreign assets rose by $3.5 billion while its foreign liabilities decreased by $3.9 billion.

NFAs represent both central bank and commercial bank assets held by non-residents, minus their liabilities.

The $17.4 billion reduction in the deficit followed a $7.04 billion reduction in February.

Before that, the central bank had been drawing on the NFAs over the past two and a half years to help support the country’s currency. In September 2021, NFAs stood at a positive $3.9 billion.

Oil Updates – prices fall for a 3rd day as Middle East ceasefire hopes rise

NEW YORK/SINGAPORE: Oil prices fell for a third day on Wednesday amid increasing hopes of a ceasefire agreement in the Middle East and rising crude inventories and production in the US, the world’s biggest oil consumer

Brent crude futures for July fell 70 cents, or 0.8 percent, to $85.63 a barrel by 7:56 a.m. Saudi time. US West Texas Intermediate crude for June declined 75 cents, or 0.9 percent, to $81.18 per barrel.

Expectations that a ceasefire agreement between Israel and Hamas could be in sight, following a renewed push led by Egypt to revive stalled negotiations between the two, pushed oil prices lower.

“The potential for a ceasefire agreement between Israel and Hamas has eased concerns of an escalation of the conflict and any possible disruptions to supply,” ANZ analysts said in a note on Wednesday.

However, Israeli Prime Minister Benjamin Netanyahu vowed on Tuesday to go ahead with a long-promised assault on the southern Gaza city of Rafah, whatever the response by Hamas to the latest proposals for a halt to the fighting and a return of Israeli hostages.

Also pressuring prices were swelling US crude oil inventories and rising crude supply.

US production rose to 13.15 million barrels per day in February from 12.58 million bpd in January, its biggest monthly increase in about 3-1/2 years, the Energy Information Administration said on Tuesday.

“Continued signs of inflation also raised concerns about demand for crude oil. This comes ahead of the US driving season, where demand for gasoline rises strongly,” analysts at ANZ said.

Keeping oil from slipping further, output by the Organization of the Petroleum Exporting Countries was seen falling by 100,000 bpd in April to 26.49 million bpd, a Reuters survey found on Tuesday.

The survey reflected lower exports from Iran, Iraq and Nigeria against a backdrop of ongoing voluntary supply cuts by some members agreed with the wider OPEC+ alliance.

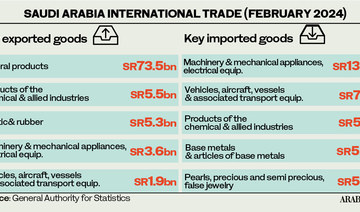

Saudi Arabia’s real GDP rises by 1.3% in first quarter: GASTAT

RIYADH: Saudi Arabia’s real gross domestic product saw a 1.3 percent rise in the first three months of this year compared to the previous quarter, official data showed.

According to the General Authority for Statistics, this rise in real GDP was propelled by oil and non-oil activities which increased by 2.4 percent and 0.5 percent during the period, respectively.

On the other hand, government activities in the Kingdom witnessed a decline of 1 percent in the first quarter of this year, compared to the last quarter of 2023.

However, GASTAT revealed that Saudi Arabia’s real GDP decreased by 1.8 percent in the first quarter of 2024 compared to the same period of the preceding year.

The authority attributed this decline to a drop in oil activities, which decreased by 10.8 percent year-on-year in the first quarter. The fall in oil exports stemmed from the Kingdom’s decision to curtail crude output, in line with an agreement by the Organization of the Petroleum Exporting Countries and its allies, collectively known as OPEC+.

In a bid to maintain market stability, Saudi Arabia decreased its oil output by 500,000 barrels per day in April 2023, a measure that has now been extended until December 2024.

Meanwhile, non-oil activities in the Kingdom witnessed a 2.8 percent year-on-year increase in the first quarter, with government activities experiencing a growth of 2 percent during the same period.

Strengthening the non-oil private sector is crucial for Saudi Arabia, as the Kingdom is steadily reducing its dependence on oil, aligned with the economic diversification efforts outlined in Vision 2030.

In March, another report released by GASTAT revealed that Saudi Arabia’s GDP decreased by 0.8 percent in 2023, compared to 2022.

On the other hand, the Kingdom’s non-oil activities demonstrated significant growth of 4.4 percent in 2023 compared to the previous year.

In 2023, the Kingdom’s government activities also witnessed a rise of 2.1 percent compared to 2022.

GASTAT releases International Trade report

On April 30, GASTAT also released its international trade report, which indicated that Saudi Arabia’s non-oil exports, including re-exports, declined 13.7 percent to SR272.37 billion ($72.62 billion) in 2023 compared to 2022.

The analysis revealed that the Kingdom’s overall merchandise exports also fell by 22.2 percent year-on-year in 2023 to SR1.2 trillion, driven by a 24.3 percent decrease in oil exports during the period.

Consequently, the percentage of oil exports out of total exports decreased to 77.3 percent in 2023 from 79.5 percent in 2022.

On the other hand, Saudi Arabia’s imports rose by 9 percent in 2023 to SR776 billion compared to the year-ago period.

The report also revealed that Saudi Arabia’s trade balance surplus stood at SR424 billion in 2023.

China was Saudi Arabia’s most important trading partner in 2023, with exports to the Asian nation amounting to SR199.3 billion or 16.6 percent of the total exports.

Japan and India closely followed China with $121.83 billion and 113.35 billion, respectively.

According to GASTAT, South Korea, the US, and the UAE, as well as Bahrain, Taiwan and Malaysia were the other countries that ranked in the top 10 destinations for Saudi Arabia’s exports.

On the other hand, imports from China to Saudi Arabia amounted to SR162.55 billion in 2023, followed by the US and the UAE with SR70.50 billion and SR50.05 billion, respectively.

India, Germany, and Japan, along with Switzerland, South Korea, and Italy, were the other countries that ranked in the top 10 countries for imports.

The report revealed that the Jeddah Islamic Port topped the list of terminals through which goods reached the Kingdom in 2023 at a value of SR227.38 billion, corresponding to 29.3 percent of the total imports.